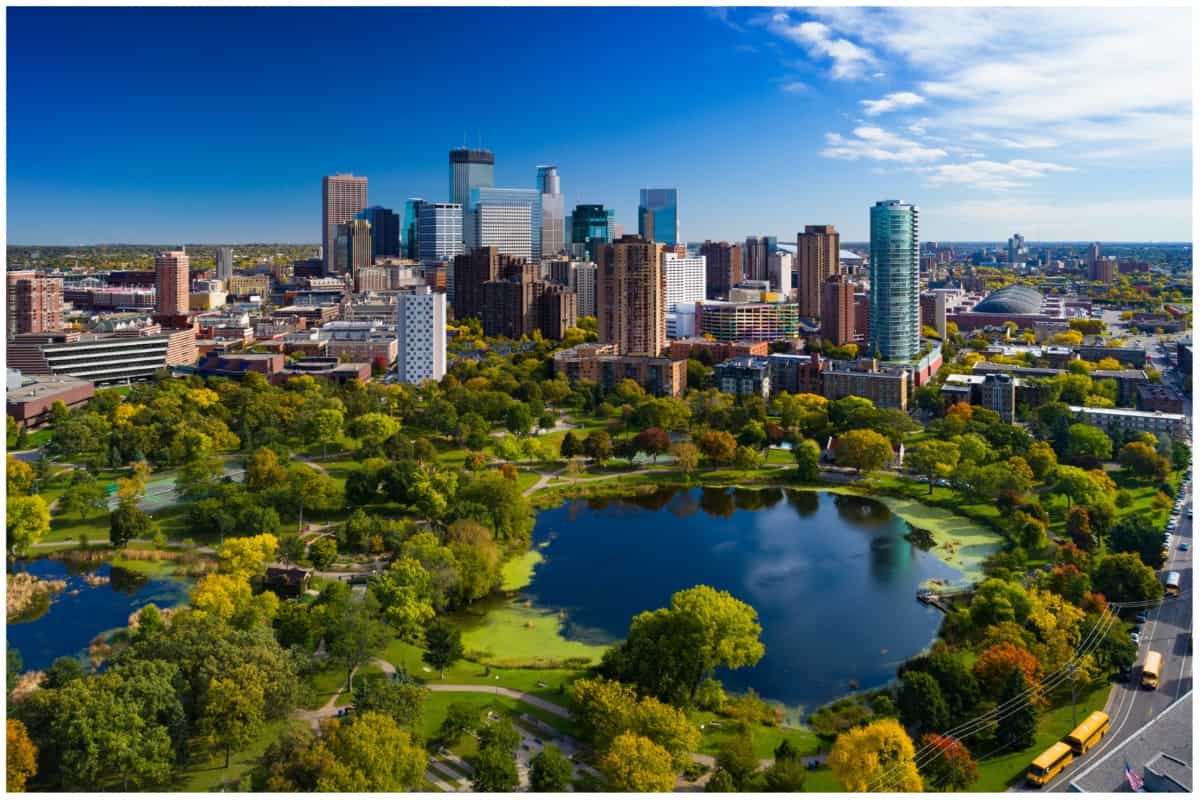

Coordinating a Minneapolis 1031 exchange identification notice inside the fixed 45-day window, from candidate screening to notice delivery.

The 45-day identification window opens on the closing date of the relinquished property and does not pause for weekends or holidays. Minneapolis investors moving through this window need a replacement property strategy already in motion before the START EXCHANGE REVIEW even closes, not one that starts from scratch once the clock begins.

There is no extension available for this deadline regardless of how complex the exchange is or how tight Minneapolis market conditions happen to be at the time. Missing it converts the entire transaction into a taxable sale, which is why identification strategy work typically begins during the marketing period for the relinquished property rather than waiting for a closing date to be confirmed.

Minneapolis exchangers sometimes treat the relinquished closing date as flexible right up until it happens, but once that date is set, the 45-day and 180-day clocks are locked regardless of anything else in the transaction. Confirming the closing date early, and building the identification plan around that specific date rather than an estimated range, removes one more variable from an already tight schedule.

Certain Minneapolis submarkets move fast enough that a property worth identifying in week one can be under contract with another buyer by week three. Industrial space along the I-494 and I-694 ring has seen this kind of turnover, and well-located multifamily-office product downtown draws similar competition.

Screening candidates early, before the 45-day clock even starts, is the main way to avoid discovering in week four that the preferred property is no longer available.

Minneapolis submarkets do not all move at the same speed, which means a screening plan built for one part of the metro can misjudge timing in another. A candidate near downtown or the North Loop may need a faster decision than a comparable property further out in the suburbs, so the screening calendar accounts for submarket-specific pace rather than treating the whole Minneapolis market as one speed.

Yes, the count runs on calendar days from the relinquished property's closing date without pausing for weekends, federal holidays, or anything else. If day 45 lands on a weekend, the deadline generally moves to the next business day, but this should be confirmed with the qualified intermediary rather than assumed.

Up to three properties can be identified regardless of their combined value under the standard rule, or more than three under the 200 percent or 95 percent rules if the investor needs a wider list. Most Minneapolis exchangers use the three-property rule unless they are deliberately keeping multiple submarkets in play.

The exchange fails and the transaction is treated as a taxable sale, with no ability to extend the deadline afterward. This is the main reason identification work starts well before the relinquished property even closes, so the window is used to confirm candidates rather than search from nothing.

No, the list is fixed once the 45-day window closes, so any property acquired afterward needs to have already appeared on that notice. This is why backup candidates are included on the original list rather than held in reserve outside of it.

Yes, in a fast-moving Minneapolis submarket, waiting until the START EXCHANGE REVIEW is under contract to start screening replacement candidates can cost real time inside the 45-day window. Early screening does not commit the investor to anything, it simply narrows the field before the clock is running.

Minneapolis 1031 exchange closing coordination that sequences lender, title, and escrow milestones against the fixed 180-day deadline.

Explore

Three property rule strategy for Minneapolis 1031 exchange investors ranking ring-industrial and retail replacement candidates before the 45-day.

Explore

How Minneapolis 1031 exchangers use the 200 percent identification rule to keep multiple submarkets and asset classes in play at once.

Explore

When Minneapolis 1031 exchangers use the 95 percent identification rule for wide portfolios, and how the acquisition threshold is tracked.

ExploreBring the sale timing, replacement goals, property candidates, and advisor questions into one Minneapolis exchange review.